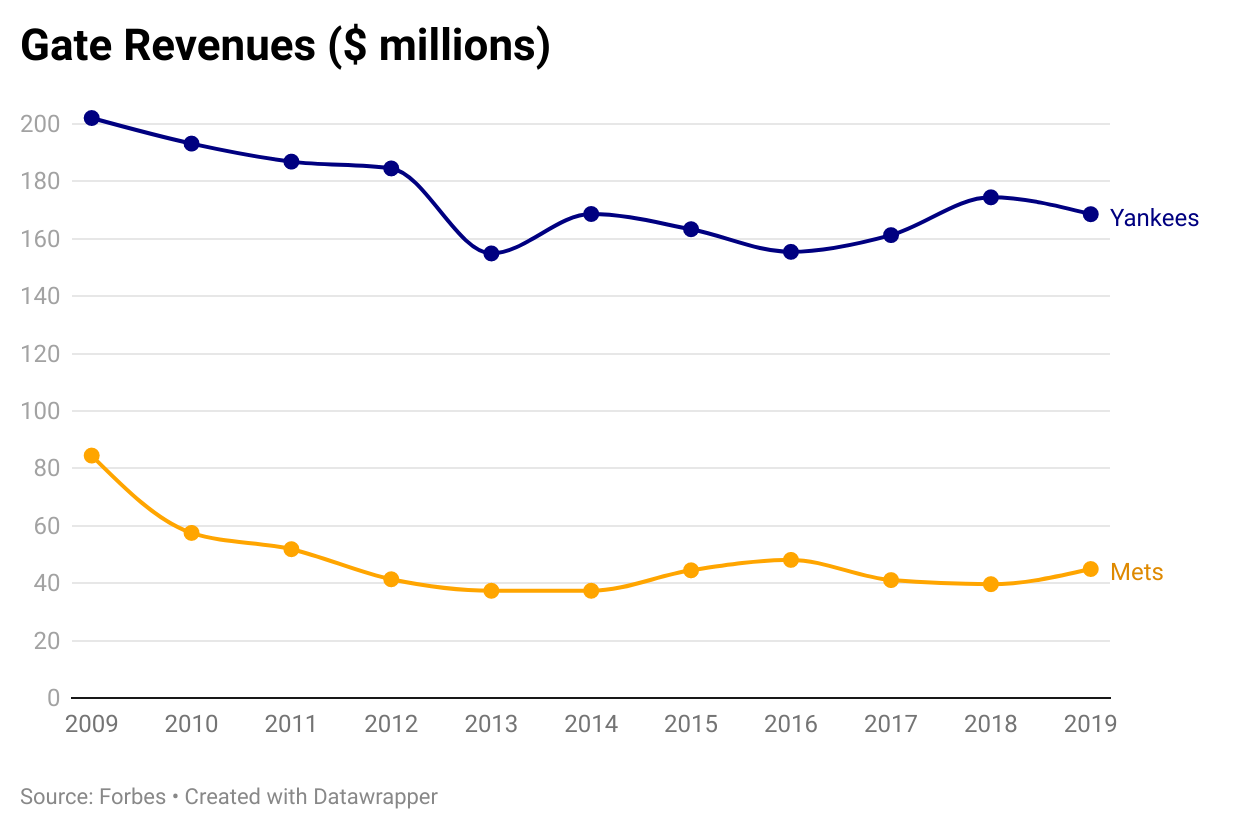

| As can be seen in the above chart, the seasons in which the teams play well produce higher gate revenues. Another benefit of better on-field play is the possibility of raising ticket prices: Fans are more likely to pay more for a ticket to watch a team in contention. The Yankees’ average ticket price from 2009 to 2019, during which they averaged 93 wins a season, was about $63; the Mets’ average ticket price over the same timespan, during which they averaged 78 wins, was roughly $27.

Cohen needs to sign Francisco Lindor, a great player in his prime at a crucial position, to a contract extension. Another shortstop, Fernando Tatis Jr., recently signed a 14-year, $340 million deal with the Padres, and the Mets should give Lindor a comparable deal because it would likely improve the team’s value.

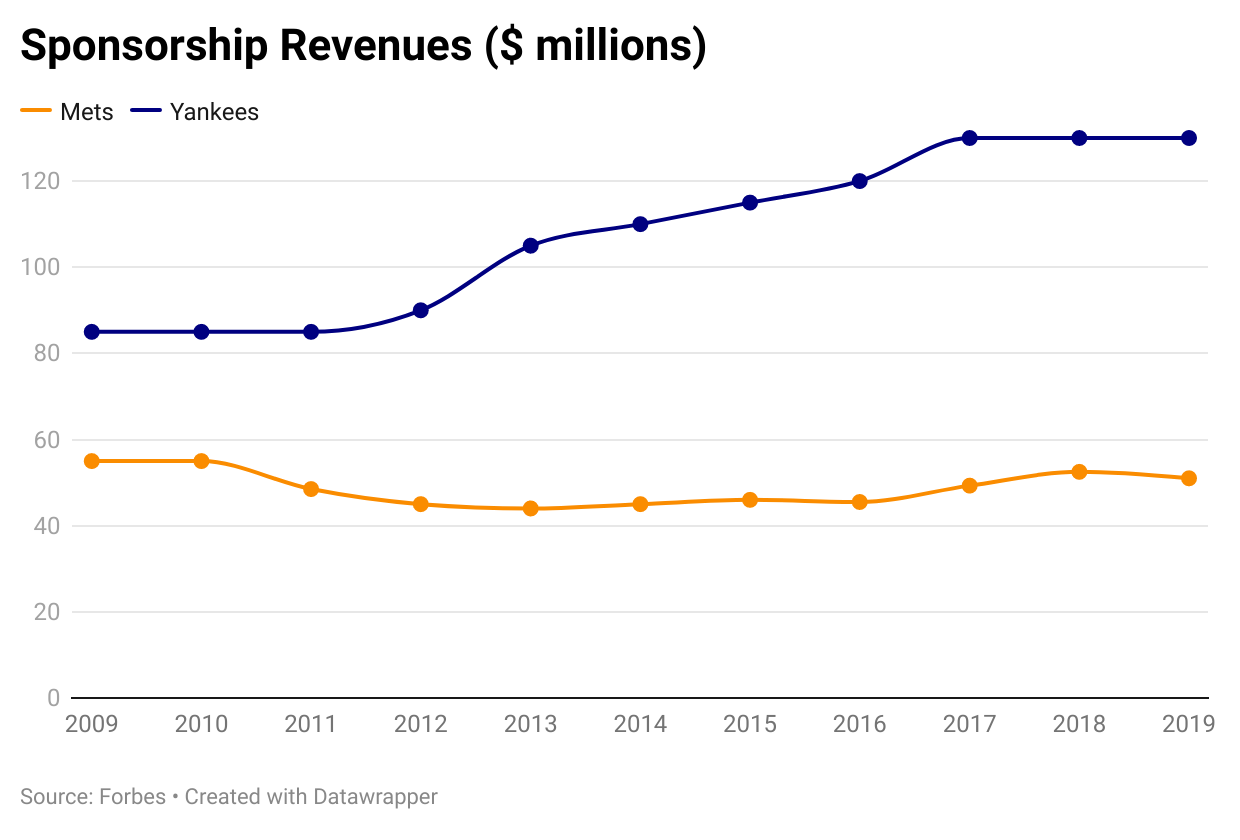

In addition, although it is not included in the chart, there is an opportunity for increased gate revenues if the club makes the playoffs. In 2015, the last time the Mets had a deep postseason run, the organization brought in an additional $17 million in gate revenue for its playoff games. And like fans, sponsors are more likely to flock to, and pay more to advertise with, teams that have a better on-field product. | |

{kind=link}