Upstart Aave shows DeFi dreams are for real

Protests. Wildfires. Pandemic. A presidential election. In these chaotic times, it can be hard to keep up with the far-out frontiers of “fintech.” Yet even amid this manic news cycle, the groundwork is being laid for an alternate financial reality. So much innovation is afoot.

The burgeoning world of decentralized finance, or “DeFi,” as its practitioners dub the cryptocurrency landscape (with more than a dollop of rebellious braggadocio), is growing neck-whippingly fast. Since the beginning of July, deposits by cryptocurrency enthusiasts into DeFi projects have swelled to more than $10 billion from $2 billion, according to DeFi Pulse, which tracks the industry’s preferred “total volume locked” metric. It has been a rocket-like rise.

In previous Ledger dispatches, we’ve introduced you to some of the leading DeFi projects benefitting from this quiet boom. Uniswap, a decentralized cryptocurrency exchange, is currently the market leader with $2.22 billion in deposits. Maker, minter of a popular so-called stablecoin, a cryptocurrency designed to maintain a fixed price peg, claims $1.82 billion in funds, making it the runnerup. In third place with $1.16 billion is Aave, a project that calls itself the “money market protocol.”

I spoke with Stani Kulechov, Aave’s chief executive and cofounder, to better understand the latest cryptocurrency craze and Aave’s place in it. When the Finnish entrepreneur talks about DeFi, and Aave’s mission in particular, he doesn’t linger on the risk and obvious associations with gambling. Instead, he sets his sight on a higher purpose.

“In some countries, the access to savings is very limited. You can save money in your national currency, but you’re losing more in terms of inflation, and that’s a very problematic thing,” Kulechov says. Aave offers an alternative, in his view, “a kind of permission-less savings account, where no one can go in between your capital and the interest that you’re earning.”

Three quarters of the people who use Aave’s software use it strictly to earn interest on deposits; thus, the money market moniker. (In the process, lenders also earn “governance tokens,” similar to corporate shares, which entitle holders to a say in the direction of the project.) The remaining quarter of users take loans from Aave, often to meet collateral obligations due elsewhere—a common occurrence in the cryptocurrency industry, where sudden price swings are the norm.

All the code and technical complexity underpinning Aave—and similar DeFi projects, like rival Compound—could be, in the long run, a gamechanger for financial inclusion, Kulechov says. It is hifalutin talk for an industry currently dominated by financial sharks and Bitcoin whales who frequently describe themselves as “degenerates.” But some investors are betting, like Kulechov, that this way the future of finance lies.

Adam Goldberg, formerly an investor at Lightspeed Ventures who has since founded his own cryptocurrency-focused investment outfit, Standard Crypto, is one such believer. He is leading a round of investment in Aave worth $25 million by purchasing a raft of the project’s own governance tokens. Goldberg reasons that DeFi’s high growth rate signals riches ahead. “It’s finance that innovates at the speed of software,” he says.

Recent macroeconomic trends bolster crypto-bulls’ arguments. Aave, which offers potentially higher yield savings than traditional banks (alongside greater risk, of course), “is particularly relevant to many people right now because of the zero-interest rate environment we are in,” Goldberg says.

At this stage of the game—and for many people, it is indeed a game—gambling on DeFi fever dreams is a surefire way to lose money. But for a new class of pros, it’s a miracle in motion. When smoke from the world’s many disasters clears, the progress being made on this revamped financial infrastructure will become readily apparent.

Robert Hackett

@rhhackett

robert.hackett@fortune.com

“We have this habit of saying that a DEX is a thing rather than an action because we are stuck in a centralized services frame of mind. Coinbase is a thing, a business, a corporation. But if the trade is actually happening peer-to-peer, then the “DEX” being “used” is just software and an internet connection. In that case, there isn’t a thing called a DEX. .”

How should regulators react to the DeFi craze and the decentralized exchanges (DEX) that enable it? Coin Center's Peter Van Valenburgh argues that, if a DEX is truly decentralized, there's nothing to regulate—only people using software. His piece is wonkish and not impartial (it's his job to shoo away the regulators), but still a good read. The piece is also a good primer on the two very different types of oversight—anti-money laundering vs securities regulation—that crypto companies face.

Content From TripActions

R.I.P. Expense Reports

Introducing TripActions Liquid™, the modern payments and expense solution that revolutionizes expense management so employees and finance teams no longer have to deal with the hassles and frustrations of expense reports, ever again.

Click here to learn more

A NOTE FROM FORTUNE'S EIC FORTUNE MPW Next Gen Community

Join the Most Powerful Women Next Gen Community, attend the October 13-14 Virtual Summit and experience 6 months of Fortune Connect! Apply now!

50%

Half of consumes are now using a challenger bank for some payments. The figure is via Capgemini's new World Payments report, which also notes 38% of consumers are using a "Big Tech" service (think Apple et al) to pay. And it's not just young people: the pandemic has seen baby boomers (age 56+) rush to embrace digital payments.

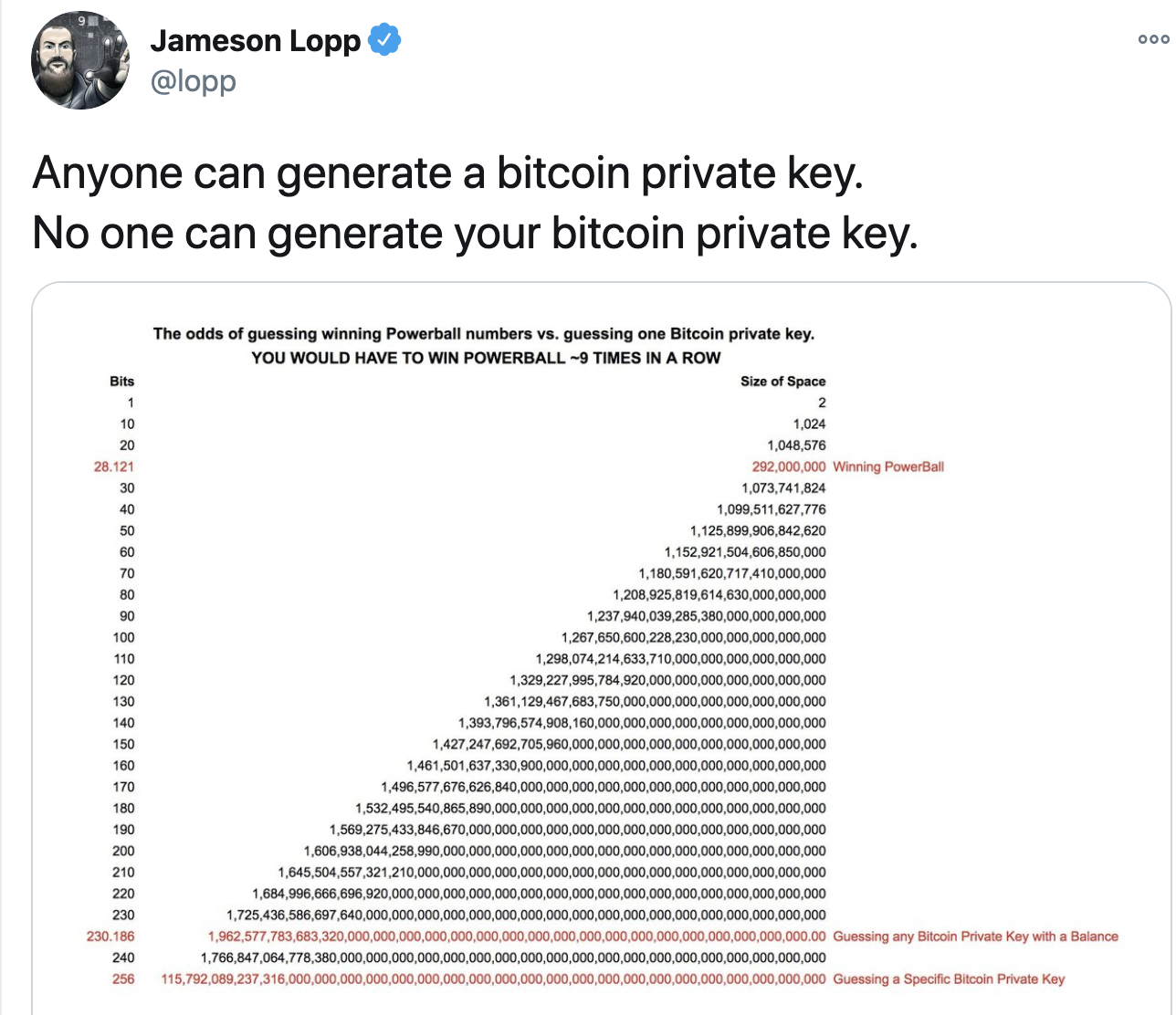

In a world where hacking and security meltdowns feel evermore common, Crypto OG Jameson Lopp reminds us of Bitcoin's incredible security protocol. He points out that the odds of guessing someone's private key are akin to winning nine PowerBall lotteries in a row.

This edition of The Ledger was curated by Jeff John Roberts. Contact him at jeff.roberts@fortune.com

Thanks for reading. If you liked this email, pay it forward. Share it with someone you know. Did someone share this with you? Sign up here. For previous editions, click here. To view all of Fortune's newsletters on the latest in business, go here. |

{kind=link}