| 25 February 2025 | View in browser |

|---|---|

|

|---|

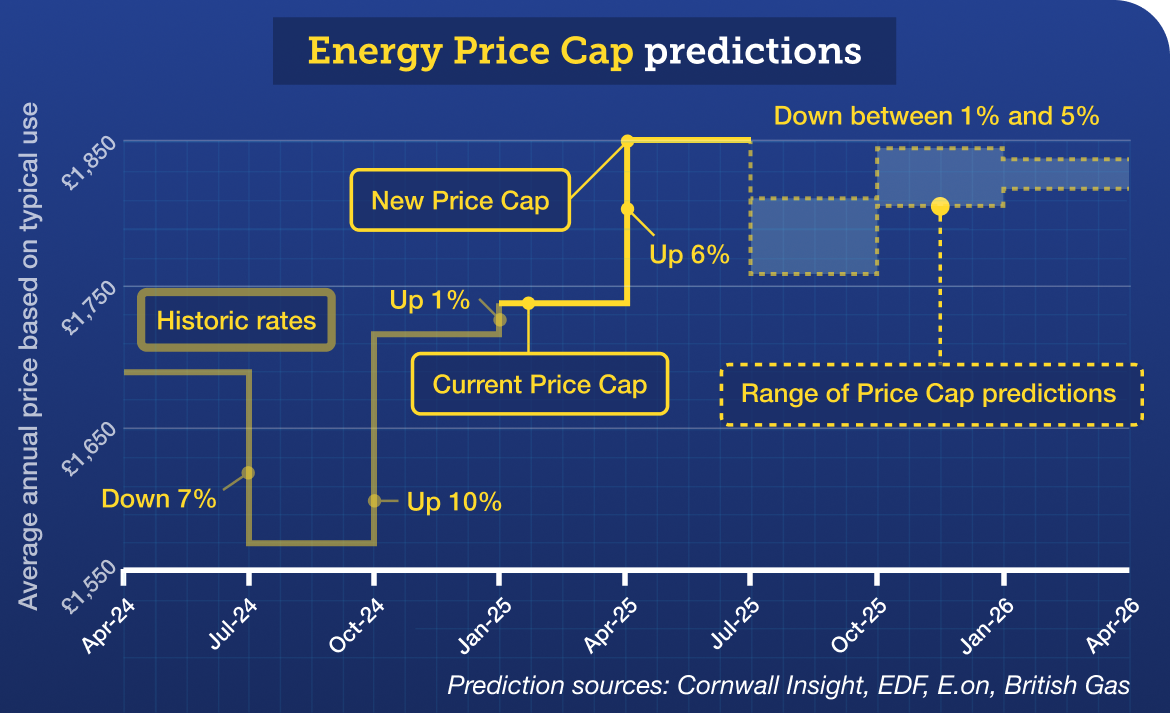

The huge bulk of the rise is on the unit rates - the amount you pay for each unit of energy. The elec standing charge is actually dropping. That means lower users will see a small rise - someone paying £100/mth dual-fuel would typically see a 5% rise - yet higher users will see a bigger rise - someone on £300/mth would typically see it up about 9%.

Q. I'm on an old-school prepay meter. Can I fix? Sadly not. While some firms allow those on smart prepay meters to fix, frustratingly none allow those on old-school key or card meters to do so. The elec-only Octopus Agile tariff's rates change half-hourly, based on wholesale prices, so much so it can be free or even pay you to use energy in the middle of the night, but very costly at peak times. It's good for those who can nimbly shift their usage to take advantage of super-cheap times or who have battery storage. Tomato Energy's Smile tariff works in a similar way. The Octopus tariffs are only available for existing customers, though to get 'em, you could first try switching to the Flexible Octopus Price Cap tariff then, once in, switch to one of these. - 'Add-on' tariffs, where you can only charge your car on the cheaper rate. Ovo and Scottish Power offer these, so you can add EV charging to whichever of their tariffs you're currently on, and you'll get a cheap rate to charge your EV at any time. All other electrical use in your home will be charged at your existing tariff rates. So if you can get a decent fixed tariff from these firms, the fact you can charge your EV even cheaper is a boon. - Two-rate tariffs giving you cheaper elec overnight. Most EV tariffs offer five to seven off-peak hours a day (typically from midnight to 5am) and charge around 7p to 10p per kilowatt hour of elec use (the current Price Cap rate is 23p to 26p). The benefit here is if you've other appliances that you can use overnight, they'll cost less too. - Energy mythbusting covers less clear-cut issues, including the thorny question of 'better to keep heating on low all day or just when needed?' - Heat the human, not the home is for those who are really struggling (though thankfully the improving weather helps too). |

|---|

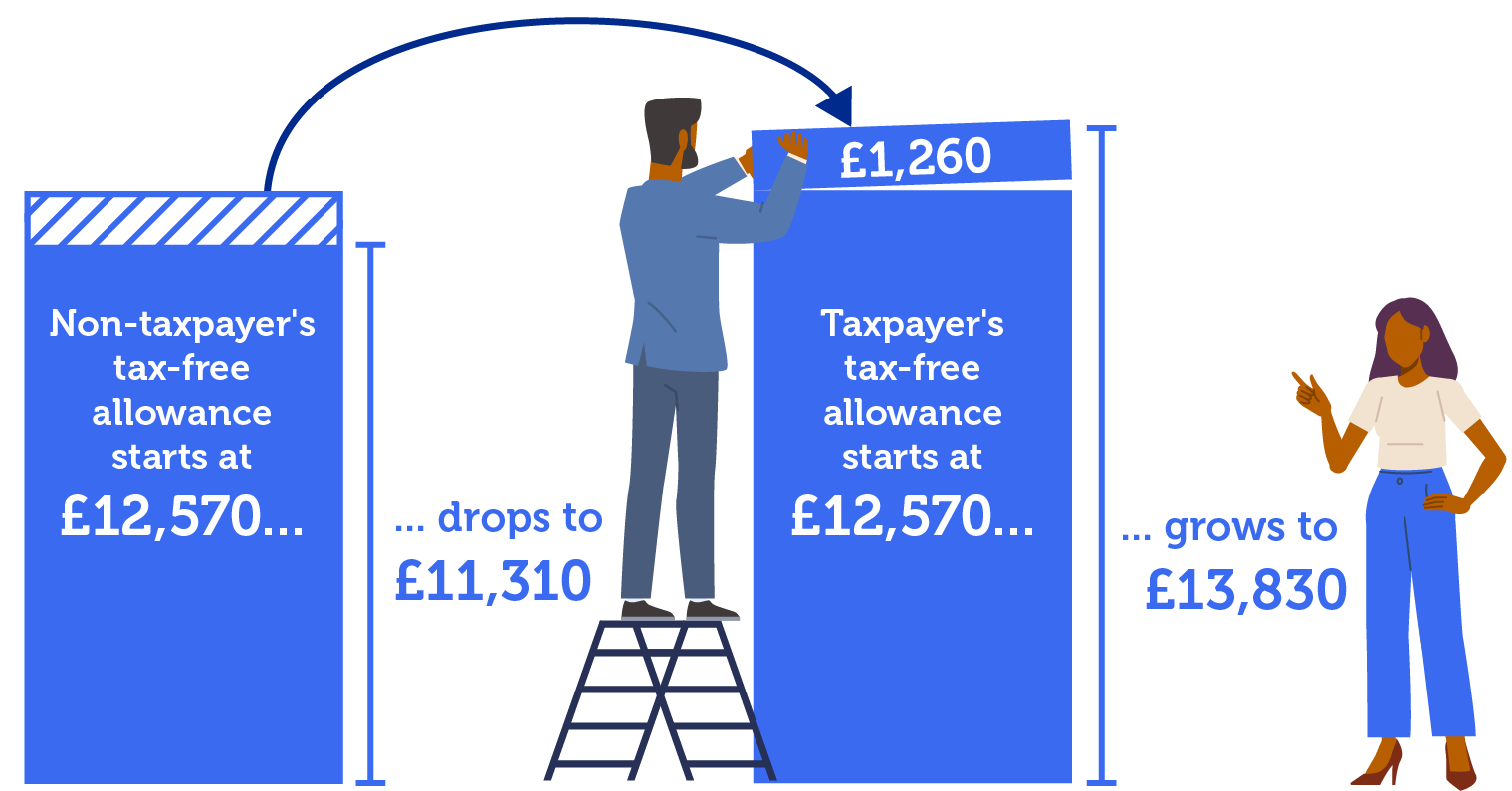

|  |  |

|---|

{kind=link}

|

So why the urgency? Well, you need to apply by the end of this tax year, 5 April, to be able to backdate to 2020/21. Leave it too late and you'll miss that £250, and the whole application system is now slower than it was...

- Just applying for this tax year (2024/25)? You can now apply again using the HM Revenue & Customs online tool.

- Applying for this AND prior tax years? For backdating, you can now only apply by post. So I'd say it's simpler to just do the current year on the same form too (though you can do the current year online and rest by post if you want).

- Just applying to backdate? You can do this if you were eligible but aren't now, but again can only apply by post.

Many are effectively being forced to use the postal system, and we've no idea how long it takes, though HM Revenue & Customs (HMRC) says as long as it's received your application by 5 April, it'll count it as applying within this tax year (for full backdating). So I'd get on with it. And possibly use signed-for delivery, as HMRC won't confirm your application has been received.

PS: Some people also find that when they apply, HMRC looks at other tax issues too, so it crystallises those. That's not a reason for not applying, as that would've happened at some point anyway.

|  |  |

|---|

| No-fee 0%: Free £175 + 5% interest:

| £7,500 to £25,000: Top easy-access savings: Monument 4.75%, min £25,000 Top one-year fix: |

|---|