| 15 April 2025 | View in browser |

|---|---|

|

|---|

| |

PS: Since we drafted the table and started pushing back on the short-term bonuses, two of the main providers offering them have now changed to much-longer one-year bonuses. - 3.8% after basic 20% tax - 2.85% after higher 40% tax - 2.61% after higher 45% tax

Fixed cash ISAs have an advantage over normal fixes. Top fixed cash ISA rates are lower than normal savings rates. Of course, for those who'd pay tax on the interest (or want to protect money in case they will in future), they're still far better. If not though, on rate alone, normal savings win. Once you've applied for the transfer, it'll move your savings over, usually within a few weeks. There are no tax-year deadlines on transfers, as your money is already in an ISA. Already got an ISA you want to transfer it into? If it allows transfers (you'll need to check), just ask for a form to do it.  Got a fixed-rate cash ISA? Check if you can ditch, switch & gain. If your fixed rate is low compared to the best today, you still have an option. You can transfer it to a new provider and pay your current fixed ISAs' interest-rate penalty for early withdrawal. Our fixed-rate cash ISA switch calculator works out if it's worth it for you. Got a fixed-rate cash ISA? Check if you can ditch, switch & gain. If your fixed rate is low compared to the best today, you still have an option. You can transfer it to a new provider and pay your current fixed ISAs' interest-rate penalty for early withdrawal. Our fixed-rate cash ISA switch calculator works out if it's worth it for you. - If the total is over the £85,000 savings safety limit, in which case you may want to spread it across a couple of providers. | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

{kind=link}

|  |  |

|---|

| | ||

|---|---|---|

| Joint-longest DEFINITE-length 0%s These two cards have identical major terms, so we've grouped them together. With both, all accepted get 32mths at 0% with a relatively low one-off fee of 3.19% (so £31.90 per £1,000 of debt shifted) for this length of card. | ||

| Long 0%, but an 'up to' with a higher fee Those pre-approved in our eligibility calc definitely get the full 32mths 0%. While it has a higher fee than the cards above, if you're pre-approved for this and not those, that's likely a price worth paying. If not, its shorter 0% is still pretty decent at 26mths. | ||

| Can you repay quicker? Low-fee DEFINITE-length 0% This 18mth card is in a sweet spot, of decent length with a low fee of just £10ish per £1,000 shifted. | ||

| Don't need too long? Longest NO-FEE 0%, but it's an 'up to' Used right, no-fee cards mean zero cost. If you're pre-approved in our eligibility calc, you'll definitely get 14mths. If not, it says 20% of customers may get the backup rate, so you may be safer going for NatWest's NO-FEE card, as while its headline 12mth 0% rate is shorter, its backup 10mth 0% rate is longer. | ||

ALWAYS follow the Balance Transfer Golden Rules:

a) Never miss the minimum monthly repayment, or you could lose the 0% deal & it'll cost far more.

b) Aim to clear the card (or balance-transfer again) before the 0% ends, or the rate rockets to the higher APR.

c) Don't spend or withdraw cash. It usually isn't at the cheap rate & withdrawals may hit your ability to access credit.

d) If you don't transfer at application, you've usually only 60 to 90 days to get the 0%. Do check your card's terms.

Q. Is it worth applying if my eligibility odds are low? | Q. What if my credit limit isn't big enough? | Q. Can I shift debt to existing cards too? | Q. Should I try to pay off my biggest debt first? SPOILER: NO.

Full help and info, including options for poorer credit scorers, in Best balance transfers.

|

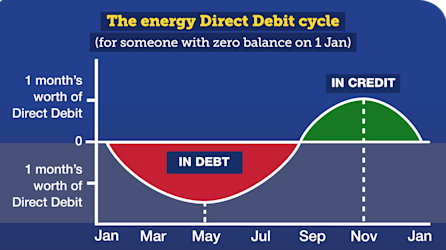

Monthly Direct Debits aim to smooth out seasonal use, so you pay the same year-round. They estimate your annual usage and, usually, divide that by 12 so you pay the same each month. That means you build up credit in the lower-use summer, and use up that credit (or go into debt) in the higher-use winter. And we're heading towards the bottom of the cycle, as late April and early May is usually when you've minimal credit/maximum debt before you start to rebuild it.

As the Energy Price Cap - which two-thirds of homes are on - has just risen 6.4% on average, some will have or will be about to see their DDs rise, so I've set my 'what's too much?' rule of thumb a little higher than it was at this time last year. Then again, as prices are predicted to drop again in July, the impact isn't huge. And just to repeat, if you're on the Price Cap, do a comparison.

|  |  |

|---|

| No-fee 0%: Barclaycard (check eligibility) up to 14mths 0%, 24.9% rep APR interest Free £150 + £36/yr cashback:

| £7,500 to £25,000: People's Choice (check eligibility), 5.8% rep APR interest Top easy-access savings: Atom Bank 4.75%, no min Top one-year fix:

|

|---|

| |

|---|