| 10 June 2025 | View in browser |

|---|---|

|

|---|

Of course you may want to stick with your existing network - in which case, if you're out of contract, benchmark the best deals from our comparison and use our how to haggle down your mobile bill guide to ask them to beat or match your bill. - iPhone 15 (128GB): 100GB/mth of data, equiv £28.08/mth over 2yrs - Samsung S25 (128GB): 100GB/mth of data, equiv £26.49/mth over 2yrs - Samsung S24 (128GB): 300GB/mth of data, equiv £24/mth over 2yrs - Samsung S23 (released 2023), 'pristine' condition: £299 - Google Pixel 8 (released 2023), 'pristine' condition: £305 - For max cash. - Want a quick, hassle-free sale? - Only got an empty mobile phone box? Don't bin it. Flog your tech leftovers online, eg, iPhone 16 Pro boxes sell for up to £16.  12. Dial a quick code to save your phone's unique ID number - the police will request this. To access it, dial this quick code then screen grab your phone's unique IMEI number (an image of one is on the right). This can then be used by the network to block or identify a phone if it's been stolen. 12. Dial a quick code to save your phone's unique ID number - the police will request this. To access it, dial this quick code then screen grab your phone's unique IMEI number (an image of one is on the right). This can then be used by the network to block or identify a phone if it's been stolen. - Remotely wipe all the data from your phone. - Remotely lock your phone (Samsung and other Android devices only). |

|---|

{kind=link}

|  |  |

|---|

| All links go via our eligibility calc so you can check acceptance odds first | |

|---|---|

- Min income? £15,000/yr. | |

(29.9% rep APR after the 0% ends) While this has a worse 0% offering than the others, less income is required to get it, and if it's the only option you've a chance of getting, 12mths is still decent for some respite. | |

| |

|---|

Q. What should I do if I've only got a low eligibility chance of getting a card, eg, 20%? If your best chance of getting a card via the eligibility calc is say 20%, then be a 'glass half full' type. Twenty per cent is better than nothing and it means two in 10 people in your circumstances WILL be accepted. Cutting debt costs is one of the most important possible uses of your credit score (usually only trumped by a mortgage application), so go for it. The worst that can happen is you get rejected, and barring a minor credit file application mark, you're no worse off.

a) Never miss the min monthly repayment (pay it by Direct Debit), or you could lose the 0% deal & it'll cost far more.

b) Aim to clear the card (or balance-transfer again) before the 0% ends, or the rate rockets to the higher APR.

c) Don't spend or withdraw cash. It usually isn't at the cheap rate & withdrawals may hit your ability to access credit.

d) If you don't do the transfer at application, you've often only 60 to 90 days to get the 0%. Check your card's terms.

Q. Can I shift debt to existing cards too? | Q. Should I try to pay off my biggest debt first? SPOILER: NO.

See full help and info in Best balance transfers.

| The Cap varies by region and payment method. For a full list, see region-by-region Price Cap info. |

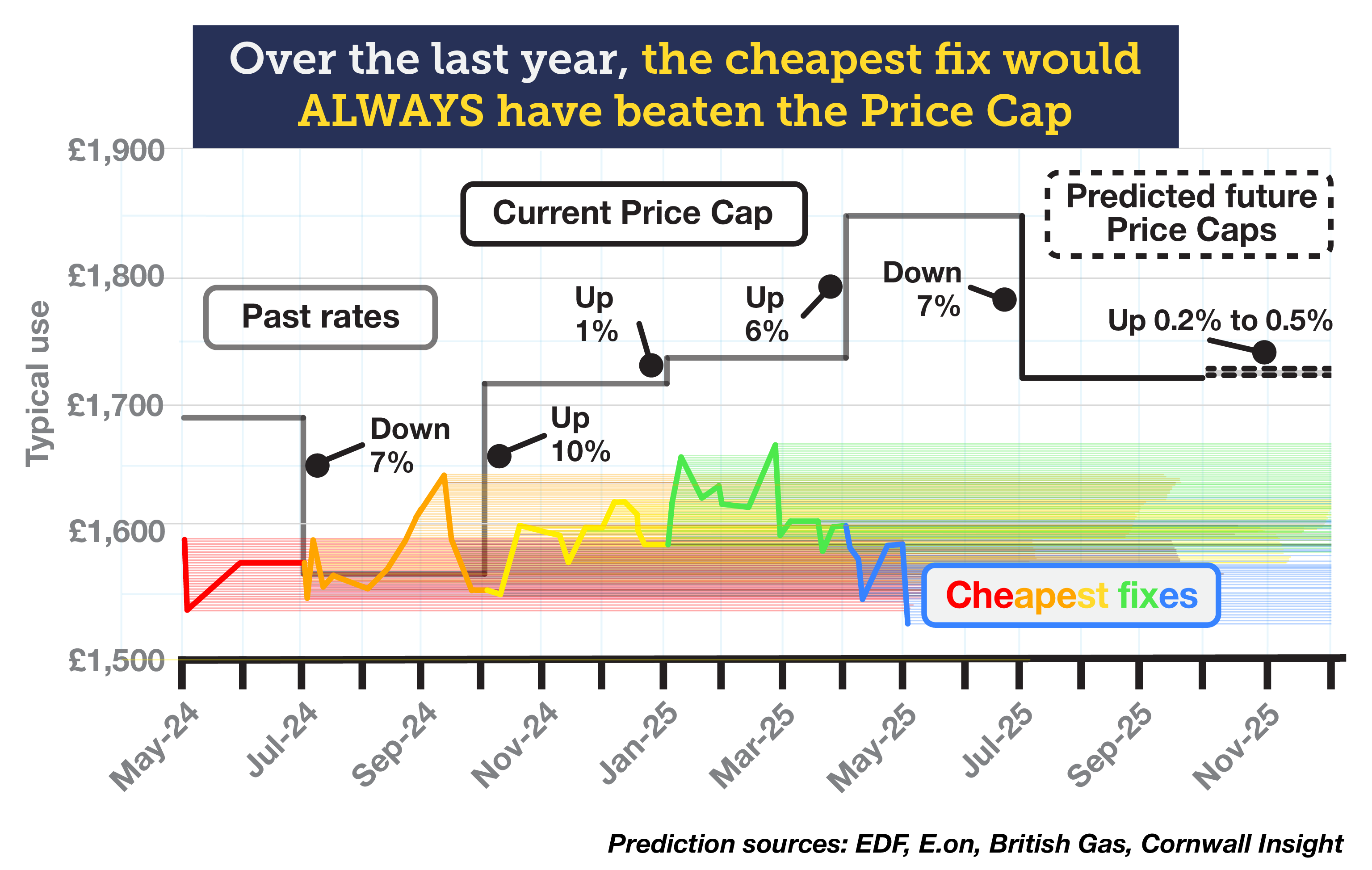

If you went for the cheapest fix (as I always push you towards), then as the infographic below shows...

|

|  |  |

|---|

| Free £100 + £15/mth cashback for 6mths: Superfast fibre (500Mb+): | Top easy-access savings: Atom Bank 4.75%, no min Top one-year fix:

|

|---|

| |

|---|